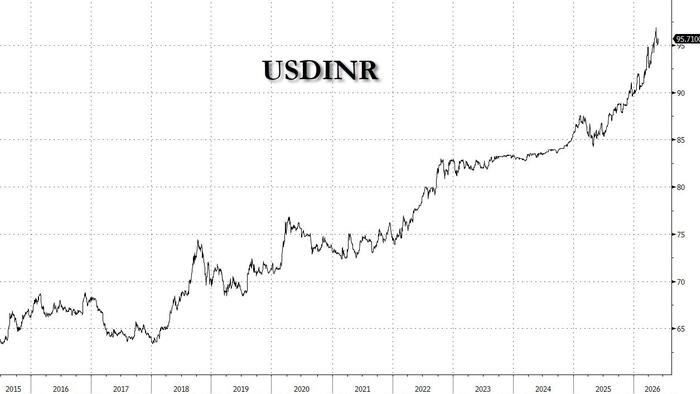

India could be on the verge of a significant foreign capital windfall, but it hinges on two policy moves that are now firmly on the table, according to Aditya Bagree, Head of Markets India at Citi.Speaking at a Citi investor conference that drew over 1,600 global clients to Mumbai, Bagree said removing the withholding tax on government bonds and securing inclusion in the Bloomberg Global AGG Index could together bring in $20–25 billion of passive, stable inflows into Indian government bond markets, a development he described as solving "a lot of issues" simultaneously.The Bloomberg Index playThe mechanics are straightforward. When foreign investors compare returns across countries, they calculate net of taxes. Strip out the withholding tax, and India's return profile improves immediately. But the bigger prize, Bagree argued, is index inclusion. Bloomberg's Global AGG Index review is scheduled for June, and if India qualifies, the resulting inflows would be passive — meaning they track the index automatically, making them more durable than discretionary bets.The benefits would ripple across multiple pressure points: a stronger balance of payments, a supportive bid for government bonds easing fiscal stress, and incremental liquidity added to the banking system.RBI rate hike debate: Citi is in the minoritySwap markets are currently pricing in four to five rate hikes over the next twelve months. Bagree pushed back firmly on that view. His argument: an interest rate defence of the rupee doesn't work unless you go very aggressive, and doing so would damage India's growth story, which is precisely what makes the country attractive to foreign capital in the first place.You Might Also Like:"A lot of the capital inflows we get is more growth-sensitive than interest rate-sensitive," he said.Citi's base case is just two hikes later in the year — and only if oil prices or a poor monsoon begin feeding through into a genuine second-order inflation problem. The current policy meeting, Bagree said, is not the moment for action.On benchmark yields, Citi's strategists see the 10-year moving toward 7.20–7.30%, reflecting global concerns about oil-driven inflation and fiscal slippage from higher subsidies. But index inclusion, if it lands, would be a meaningful counterweight.Rupee: Event-driven, not structurally brokenOn the rupee, Bagree was careful to separate noise from fundamentals. India's current account deficit is expected to widen to around 2% of GDP on higher oil prices, uncomfortable but well within historical experience. Inflation remains below target. Growth remains among the strongest of any large economy.You Might Also Like:His read on RBI's intervention approach was equally measured: the central bank is right not to defend a specific rupee level, but it does have both the mandate and the reserves to prevent excessive volatility from spilling into the real economy.The "anti-AI trade" narrative: Citi doesn't buy itOne framing that has gained traction to explain FPI outflows from India — that global money is rotating into AI-linked economies like the US, Taiwan, and South Korea and away from service-export nations like India — drew a pointed rebuttal from Bagree."I do not understand this anti-AI trade rhetoric," he said. Investors allocate to where they see growth. Countries benefiting from semiconductor demand and AI capex are seeing inflows because of real capital expenditure-driven growth — not because India is being penalised. It is a relative valuation call, not an ideological one.The longer-term India thesis, he concluded, remains intact: strong reforms momentum, new FTAs, eased FDI rules in insurance, and relaxed ECB regulations are all quietly building a more investable architecture — one that the 1,600 global investors at the Mumbai conference were clearly still paying attention to.You Might Also Like:

Withholding tax removal could unlock $25 billion in bond Inflows, says Citi's Aditya Bagree

India anticipates substantial foreign investment. Two key policy shifts, removing withholding tax on government bonds and inclusion in the Bloomberg Global AGG Index, could attract billions. This influx would strengthen India's balance of payments and ease fiscal pressures. Citi believes these developments will boost the Indian economy, making it more attractive to global investors.

594 words~3 min read