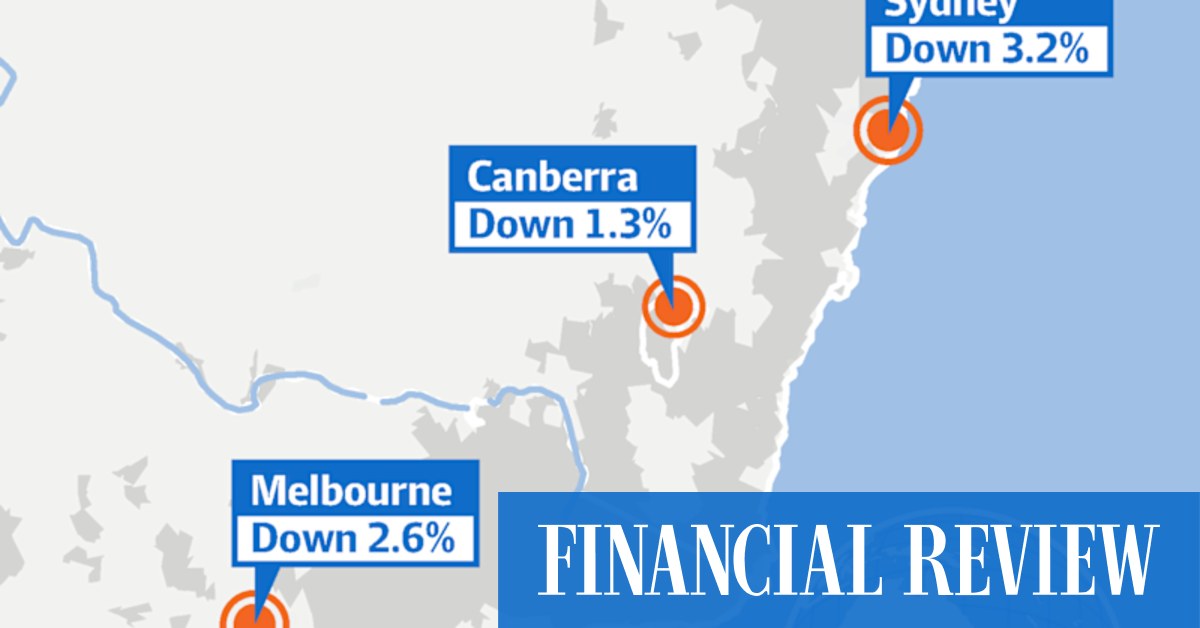

House prices in Sydney and Melbourne are down by 3.1% and 3.5% respectively, from their most recent peaks, according to the latest data from Cotality. Across Australia as a whole, house prices didn’t rise last month, the first time that has happened since January 2023. And the annual rate of house price inflation dropped to 9.5% from a most recent peak of 10.9% over the year to February.If these reports were about any of the other 86 classes of goods and services into which Australia’s consumer price index is divided, they would be greeted with universal approbation, and the government would be claiming credit for “easing cost-of-living pressures”.But because they are about the price of housing, the reaction of most politicians, much of the media and a good deal of the general public has been very different – ranging from “the sky is falling in” and “the government ought to do something to stop house prices from falling” to “it’s not our fault”.And this tells us something profoundly important about why housing affordability has deteriorated so much – and why home ownership rates among people aged under 45 have fallen so far – over the past three decades.In the decades after the second world war, Australians and their political representatives saw housing primarily as something that met basic human needs for shelter, security and a stake in the communities in which they lived. In his 1942 radio address entitled The Forgotten People – which the Liberal party holds as a sacred text – Robert Menzies spoke at length about “homes material, homes human, and homes spiritual”, about how “the home is the foundation of sanity and sobriety”, and about how the health of the home “determines the health of society as a whole”.But over the past three-and-a-half decades Australians have come to think of housing not as something that meets these basic human needs, but rather as a vehicle for accumulating wealth – or, as it is commonly put these days, “getting ahead”.Which, more than anything else, explains why we have not been able to solve our “housing affordability problem” or reverse the decline in home ownership that has now been in train for 60 years: because a very large majority of Australians do not want it to be solved, and politicians of all stripes know it.That’s why, during last year’s federal election campaign – despite it ostensibly being about the “cost of living”, and despite the fact the cost of housing is the largest single component of the “cost of living” – the leaders of both major parties said they wanted house prices to keep going up. And both major parties promised policies which would produce that result – the 5% deposit scheme in Labor’s case and the super for housing proposal on the Coalition’s.One of the contributors to the deterioration in housing affordability over the past quarter-century (not the only one, and not necessarily the most important one) has been the growing presence of investors in the housing market.Graph showing share of new home loans belonging to investors v first home buyers v other owner occupiersThe change to the capital gains tax regime in 1999 greatly enhanced the appeal of negative gearing by transforming it from a strategy that had hitherto been primarily about deferring tax, to one that facilitated both deferring and permanently reducing tax, by in effect converting wage and salary income, taxable at full marginal rates in the year in which it was earned, into capital gains taxable at half marginal rates in a year of an investor’s choosing.As a result, the proportion of individuals who had property investments rose from 15% in 1999 to over 20% during the 2010s; the proportion of those who were “negatively geared” rose from 51% in 1999 to over 70% by 2008, before declining interest rates made it increasingly difficult to be negatively geared; and the proportion of housing finance going to investors rose from 26% in the second half of the 1990s to over 45% by the mid-2010s. And more than 80% of that lending to investors went to the purchase of established housing – that is, housing that we already have – serving only to push up the price of that housing and increase the demand for rental housing by outbidding aspiring homebuyers.The changes to negative gearing and the capital gains tax regime announced in the budget will, if passed by the parliament, reduce the demand for established housing from investors. And that’s a good thing, not something to be bemoaned. It will reduce the competition aspiring first home buyers face, when seeking to buy a home, from investors who can write off their interest costs against their other taxable income.Those changes aren’t responsible for the declines in house prices that have occurred in Sydney and Melbourne since the turn of the year, nor for the ease in house price inflation that has occurred elsewhere in recent months. Those things are, rather, primarily due to the three increases in interest rates which have occurred so far this year and to widespread expectations that there may be at least one more increase in the second half of this year.Interest rates will eventually come down again and house prices will eventually go up again, especially if housing supply continues to grow at a slower rate than housing demand. But if dampening the demand from investors for the housing we already have reduces the rate at which house prices go up, that should be celebrated, not bewailed.

House prices are falling in Australia. That’s a good thing – if you believe housing is a basic human need | Saul Eslake

Labor’s budget changes are not to blame for the recent dip in property prices. But the changes will help move housing away from investors – and that should be celebrated

TL;DRAI

House prices in Sydney-Melbourne fell 3-3.5%, first stagnation since January 2023. Politicians resist affordability solutions as 45% of mortgages finance investor purchases that outbid first-time buyers, sustaining artificial price inflation.

933 words~4 min read