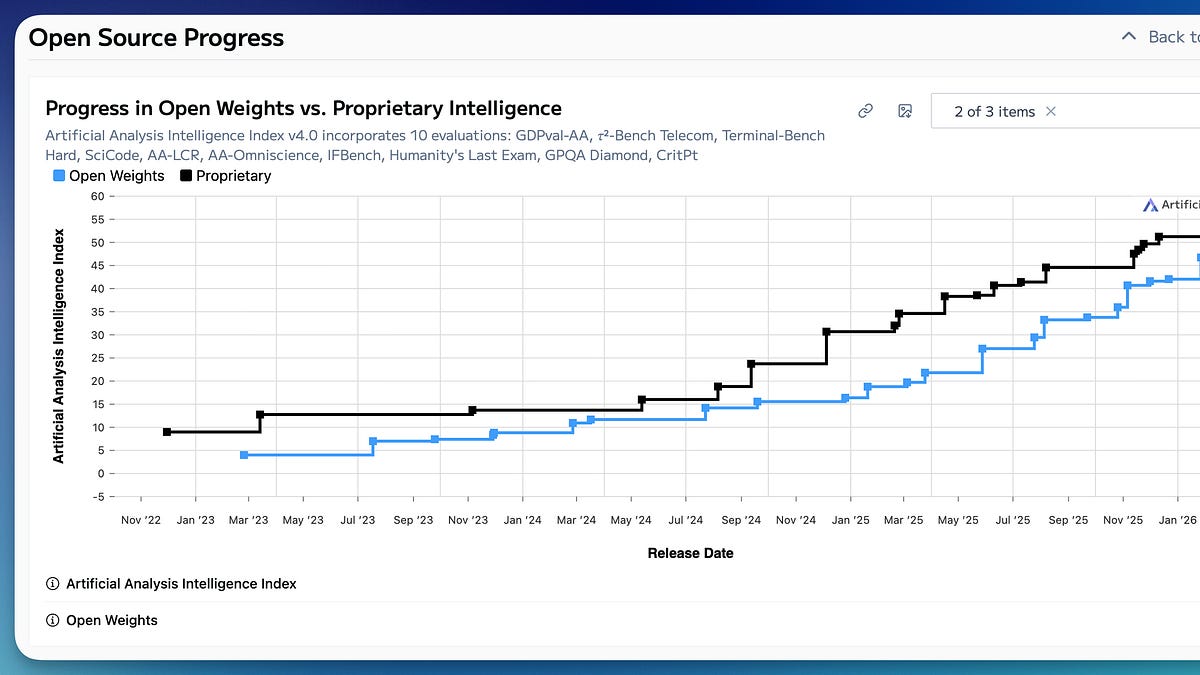

The largest debate that’ll define the future balance of power between the open and closed AI model ecosystems is primarily economic — it’s if users of AI will continue to pay dramatically more, i.e. large margins, for the top closed models. Early 2026 is a seminal time for the AI industry, as the coding agents1 have shown the first area where a huge AI market will continue to pay a substantial premium for better intelligence. The other side of this dichotomy is the inevitable decay of API businesses at these same labs. These labs will realize they need to protect their best models, rolling them out later in APIs to both protect token supply, avoid distillation, and stick to use-cases with higher margins. All of these effects will be clearly visible in 5-10 year timelines, as in the near term markets, prices, margins, and demand will be dictated by a rapid buildout of compute (supply-limited in the near term) and mass subsidization of tokens (through continued investment in new AI companies).ShareThe core of this argument rests in the obvious habit changes that are setting in with coding agents past the Opus 4.5 and Codex 5.2 thresholds. People are not making this switch because they are lazy, but because their net output is obviously higher when using an agent as an implementation aid for complex knowledge work. For people who rely on coding agents to work, they will always pay more for the best rather than settle for good enough. There are so many ways to make the product better, speed, intelligence, specialized models, etc. I would pay $2000/month for the tools today, especially knowing they’ll get much better. At the same time, it is likely that many companies are forcing agents and usage onto people that actually will get very little out of them in their current form, which helps the AI buildout (or bubble) continue.The best closed labs — right now this list is just Anthropic and OpenAI, but it’s reasonable to expect Google to catch up — will always make the most efficient models for intelligence at a given cost. Building models is a mass capital investment of talent, data, and compute. These systems, a combination of model weights, harnesses, tools, and serving infrastructure have massive returns on integration (where open models are designed to work across many, diverse serving situations). These integration benefits — the integration of hardware and new forms of software — can be expressed in any possible way of making models better. The models in the near future may saturate on benchmark scores, but if that intelligence ceiling really is a cap on utility then the labs will optimize utility per second or per watt, serving users in another way. Improving the models is possible in every direction — there have been no walls in progress. We’re early in the mass buildout of intelligence, which involves harnessing the physical world to build numerous datacenters, organizing many AI researchers so that a large team can contribute to one model, and of course solving many small, low-level puzzles that unlock performance. Every indication is that there is still meaningful performance to be unlocked and the closed labs are the best set up to extract it.The collective wisdom of the labs is that making the models smarter, in terms of the frontier of absolute intelligence, has the most value. This is the right call to me because it unlocks large new markets. Optimizing models at a fixed intelligence level locks in markets, expands accessibility over time, and increases return on investment for users (while potentially lowering margins for selling intelligence).Many people are making this bet that models will keep getting better and are learning to work well in these harnesses, even though some workflows are still a bit clunky. This is the right bet. These people all will continue to use the absolutely best models available. It’s like buying an iPhone as a consumer. You could get an Android and suffer from a bunch of paper cuts to save money, but why would you? The returns to performance are even higher in the workplace, which drives pricing power.In this mental model, the frontier labs as businesses, will look like new, reimagined forms of a mix of Apple and Microsoft. The Apple side is that they’re selling an integrated, extremely hard to replicate technology. The Microsoft side is selling high-leverage subscriptions across the economy. In 5-10 years I expect both OpenAI and Anthropic to be valued in the $2-10T range. The true frontier labs will be an oligopoly that looks like the cloud market today.On the other side of this equation is the open model economy. This isn’t to say that the frontier labs will dominate all aspects of AI use. Yes, I expect OpenAI and Anthropic to be the most representative companies of the AI boom (new companies, alongside Nvidia of course), but the collective value capture around open models will be far bigger overall, it’s just that the revenue and margins will be shared across a wide stack of companies.Many businesses want to switch to open models but the models today are not good enough in out-of-distribution tasks. Eventually open model builders will stop chasing Claude and GPT on the Artificial Analysis index and fill this niche. This fork could be driven by economic factors, where they no longer have the revenue to support the growing R&D costs for continuing to scale models. It can also be driven by pure demand, where certain AI solutions only can exist at low price points present in open models. Where closed labs are an oligopoly, open model builders and users will be far more diverse and numerous. The total market value will dramatically exceed the cumulative value of OpenAI and Anthropic.Open models are by their nature not integrated, so they will rely on multiple companies coordinating to serve them. Each of these layers will have alternatives, driving prices down to commodity pricing. These low, predictable prices will be where many enterprises enter to build in-house agents and tools for niche tasks. The predominant mode of deployment here is that enterprises find a model that hits a sufficient performance threshold on a task of interest and does not replace the model later (setup costs are high). As customizing models becomes easier, again in the open model finetuning stack we are seeing emerge (Tinker, Fireworks, Prime Intellect, etc.), this market becomes even bigger.What this will look like in the coming years is a steady rise in open model inference proportion across the entrenched hyper-scale clouds of Google, Amazon, Microsoft and new AI infrastructure companies of Together, Fireworks, OpenRouter, etc when compared to OpenAI and Anthropic.The key is that the open and closed model economies are operating on different exponentials. I still believe that progress will continue at a fast pace across the entire ecosystem, but claims of recursive self improvement (RSI) giving the closed labs an unassailable advantage are overblown. New forms of products like background agents can support both these open and closed models.The closed models hit incredible product-market fit with the current agents, starting their integrated exponential by monetizing the top end of the knowledge work. The open model economy will take far longer, but it will also be far more satisfying to follow, as it tracks the broader diffusion of AI into the entire economy and world.1The term coding agent is funny because we barely write code in them. They’re general agents that are so capable because they write a lot of code.

Open and closed models are on different exponentials

Where marginally higher intelligence drives value, and where it doesn't.

1,255 words~6 min read