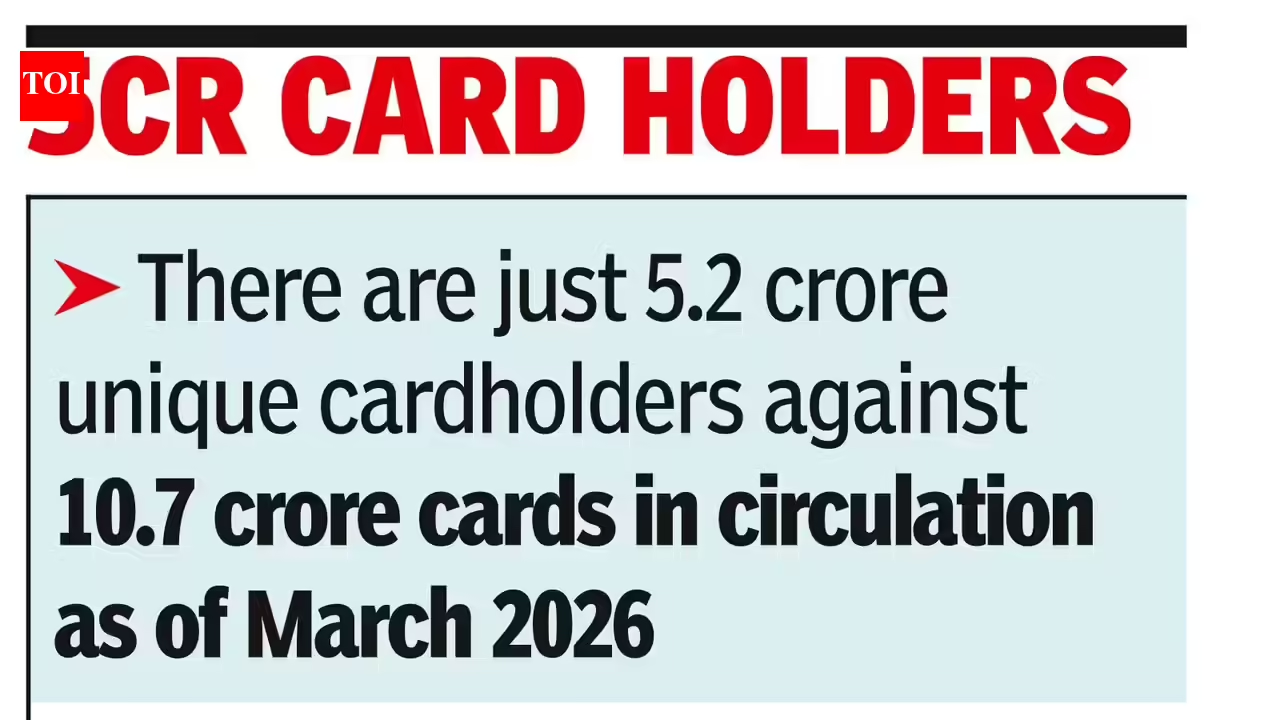

Weeks before the end of fiscal 2025–26, many credit card issuers announced or implemented significant changes to their reward structures. These included some banks overhauling points redemption limits, linking points accumulation to spending tiers, and devaluing some cards by revoking or restricting perks.In most cases, banks introduce these cutbacks once they have acquired a sizeable customer base or when the perks in question start taking a toll on their revenues.Vinit Bajaj, Group Head—Cards, Axis Bank, sees it differently. “We would like to refer to it as reward recalibration, and not devaluation; and this recent wave reflects a broader shift from broad-based, high-cost benefits to more targeted, usage-linked reward structures,” he explains.As a cardholder, the need of the hour is to visit your issuer’s portal and review the changes applicable to your card. For instance, State Bank of India’s (SBI) Cashback card still earns a 5% cashback on online expenditures and 1% on offline spends, but these monthly yields are now capped at ₹2,000 in each category—i.e. users cannot earn a cashback over ₹4,000 in a month. For holders of HDFC Bank’s mid-tier Regalia Gold, the three visits to domestic airport lounges per calendar year quarter are now conditional on a minimum expenditure of ₹60,000 in the preceding three-month period. Meanwhile, users of Kotak Mahindra Bank’s top-tier White Reserve continue to receive a 1% fuel surcharge waiver, but the cumulative relief is capped at ₹4,500 per calendar year.You would rightly feel that the rewards linked to your credit card have depreciated but resist the urge to turn scissor-happy and cut the plastic or metal in your wallet into pieces. Tweaking your monthly spending and using your reward points with a long-term view can best help you play the hand you have been dealt.

Banks are cutting credit card perks quietly; Learn how to get more value from your wallet - The Economic Times

Many banks have recently reduced credit card rewards, cashback limits, and perks, prompting cardholders to reassess their spending strategies. Experts advise optimising existing cards rather than cancelling them, diversifying across 2–3 cards, and using rewards strategically. Linking RuPay credit cards to UPI can boost benefits on everyday transactions. Ultimately, maximising value depends on understanding card features and aligning spending with reward structures.

2,149 words~10 min read