A few years ago, receiving a payment from overseas felt surprisingly complicated for something that should have been simple.

A client in the US would send $1,000. Somewhere between their bank account and yours, fees appeared, exchange rates became fuzzy, and the final amount credited often felt like a mystery. If you were a freelancer, SaaS founder, exporter, consultant, or agency owner, you probably accepted this as "just how international payments work."

Today, that assumption is being challenged.

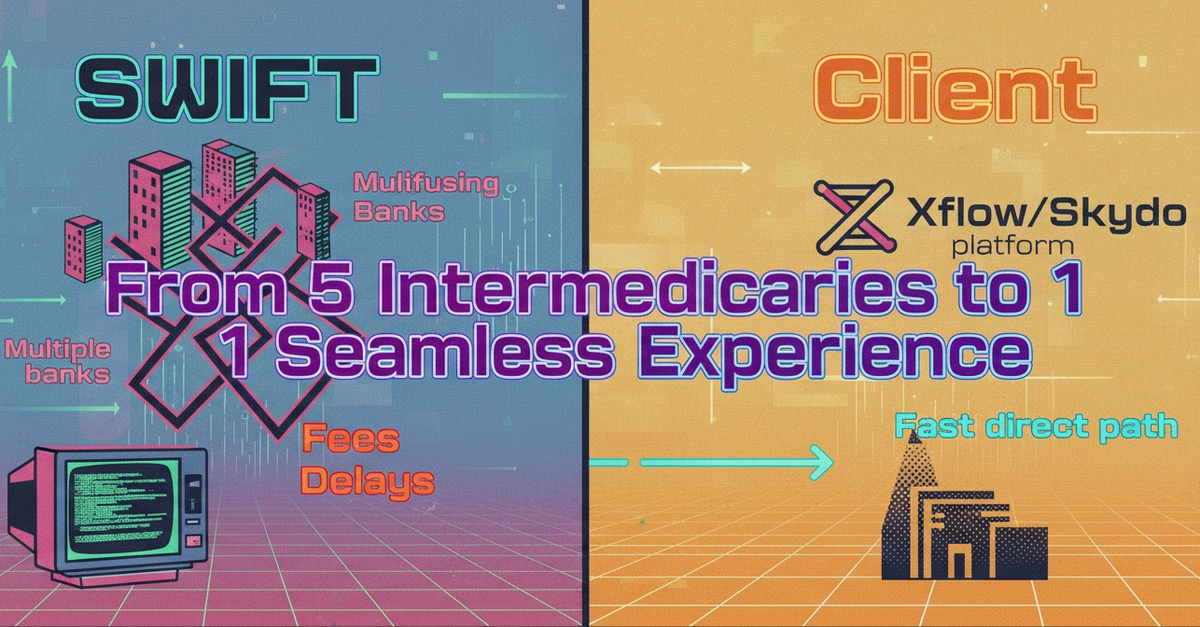

Companies like Xflow, Skydo, and several newer fintech players are making international collections faster, cheaper, and far more transparent. What's interesting is that this wasn't caused by one dramatic RBI announcement. Instead, it was the result of multiple regulatory changes that quietly transformed the landscape over the past decade.

The World Before Fintech Entered Cross Border Payments