1. The recent escalation of conflict in the Middle East has intensified a global competition over critical minerals, which are vital for advanced military hardware and defense technologies. The price of tungsten—a key input for armor-piercing munitions and missile counterweights—has soared to a European benchmark of $2,250 per ton, marking a 557% increase over the past year, a growth much faster than that seen in gold or silver. Several other “war metals,” such as germanium, antimony, tantalum, and niobium, have also seen dramatic price surges as demand rises amidst continuing conflict between Iran, the U.S., and Israel. This “war metals” phenomenon reflects shifting priorities as military production accelerates resource shortages, impacting global markets well beyond the energy transition[para. 1][para. 2][para. 3][para. 4].2. Looking ahead, the International Energy Agency projects that by 2040, global demand for lithium could increase fivefold, with graphite and nickel demand doubling. Cobalt and rare earth demand may rise 50–60%, while copper usage is expected to grow by roughly 30%. Such growth, combined with the high-intensity warfare depleting existing inventories and integrating technologies like AI and drones, intensifies the scramble for stockpiles. Responding to these pressures, the U.S. Department of Defense in October 2025 sought up to $1 billion in critical minerals for strategic reserves—spanning investments in cobalt, antimony, tantalum, and scandium[para. 4][para. 5][para. 6][para. 7][para. 8].3. Heightened mineral demand is now a cornerstone of national defense policy, linking energy security directly to strategic autonomy. Analysts point out that a stable supply of metals is no longer just an economic concern, but a factor in military competitiveness. The global race over critical minerals now encompasses not only mining rights, but also transport security and commodity pricing, making supply chain control a priority measure of national strength[para. 9][para. 10][para. 11].4. Recent reports underline the U.S. military’s vulnerability in the event of protracted wars, highlighting shortfalls in tungsten, antimony, gallium, and germanium—key elements for weapons manufacturing. Before launching strikes on Iran in early 2026, the U.S. surveyed domestic mining firms regarding the speed of ramping up production of tungsten and other crucial metals. Policy makers are scrambling to diversify supply chains and mitigate these risks through global partnerships and new strategies, such as the December 2025 National Security Strategy and the establishment of a new Forum for Resource Geostrategic Cooperation and Project Vault, a $12 billion stockpiling initiative[para. 12][para. 13][para. 14][para. 15][para. 16][para. 17].5. Reducing dependence on China is a major driver behind U.S. policy, as China dominates global critical mineral processing—with control over 60–70% of antimony, 80% of tungsten, over 90% of gallium, and the majority of rare earth refining. The U.S. is pushing diplomatic initiatives and investments abroad, particularly in Africa. Recent agreements with the Democratic Republic of Congo (DRC), a cobalt powerhouse, aim to secure American access to vital minerals while reducing Chinese influence[para. 18][para. 19][para. 20][para. 21][para. 22][para. 23][para. 24][para. 25][para. 26].6. Mining projects often require years to develop and are susceptible to market volatility. The Trump administration has taken a more interventionist stance, investing over $30 billion in mineral projects and adopting a government equity investment model, but most domestic operations won’t begin until after 2028. U.S.-backed consortia have secured priority access to DRC mineral assets, challenging China’s leading role in the region. Such competition has fueled resource nationalism across resource-rich nations, who seek to capitalize on major powers’ rivalry[para. 27][para. 28][para. 29][para. 30][para. 31][para. 32][para. 33][para. 34][para. 35].7. As land-based resources become more contested, attention is turning to deep-sea mining—a frontier valued at $177 trillion (with $81 trillion in metals). Although hampered by high costs and nascent technology, the sector is projected to scale up rapidly around 2027 and reach cost-parity with terrestrial mining by 2033. The U.S. has sped up the approval process for deep-sea mining and aims to begin pilot extraction as early as 2027, potentially bypassing future regulations from the International Seabed Authority (ISA), raising concerns of a “Wild West” rush on the ocean floor by multiple global powers[para. 36][para. 37][para. 38][para. 39][para. 40][para. 41][para. 42][para. 43][para. 44][para. 45].AI generated, for reference only

In Depth: How the Iran War Set Off a Global Scramble for Strategic Metals

The conflict has sent prices of ‘war metals’ like nickel and cobalt soaring, accelerating a global race to control the minerals critical for making everything from missiles to AI

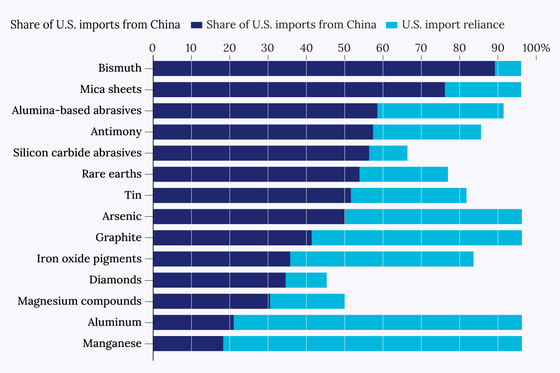

673 words~3 min read