New analysis from our Battery StorageTech Bankability Ratings Report shows that suppliers with higher exposure to energy storage revenue generally recorded stronger overall growth in 2025, as global ESS deployments accelerated and overseas markets expanded. The report evaluates the bankability based on a comparative analysis of two key components: financial and manufacturing, with industry leading figures required in order to reach the top tiers.

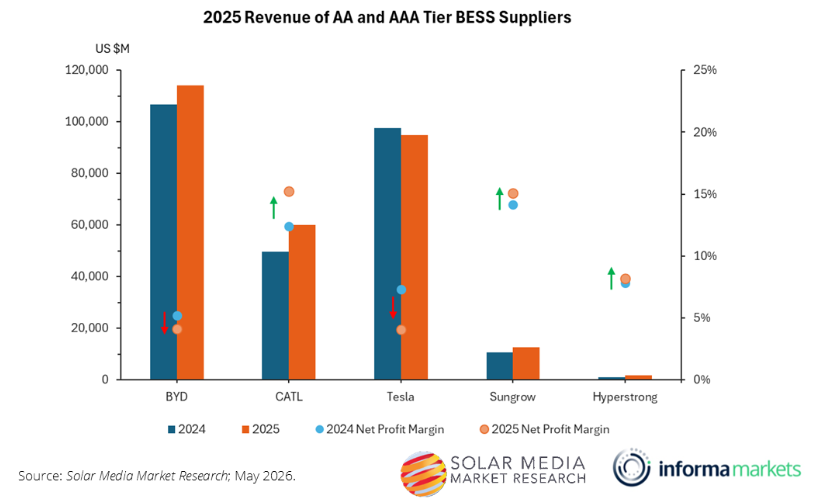

The majority of suppliers in the top two tiers of the bankability pyramid do not have energy storage as their main source of revenue, and while ESS share of total revenue has generally been increasing across all suppliers in the pyramid, CATL stands out as having this proportion fall slightly in 2025 to 15%. However, total ESS revenue did increase 9%.

Among the five top suppliers, Sungrow recorded the largest increase in ESS revenue last year, up around 49%, which accounted for nearly 42% of total revenue, while PV inverter sales increased only 6.9%. While the company has already cemented its place on the global stage for both PV and ESS with the delivery of multiple large-scale projects, 2025 saw this global approach pushed further. Revenue from mainland China declined 15%, while overseas revenue share jumped from 46% in 2024 to around 60%.