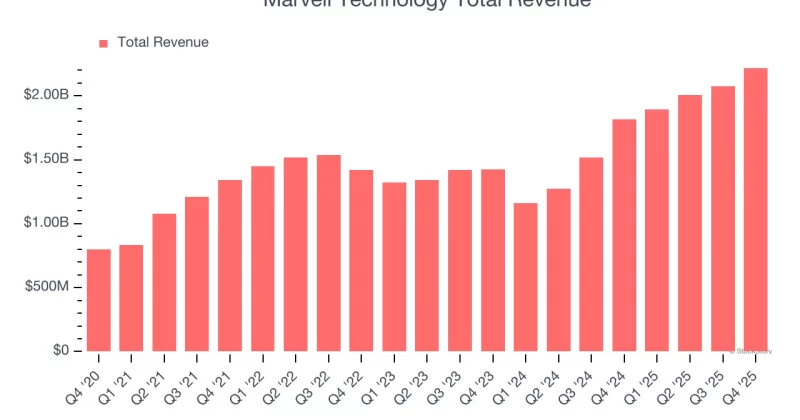

John Maynard Keynes famously said, "Markets can remain irrational longer than you can remain solvent."That's good advice for anyone looking to short chip stocks based simply on price action.I happen to like one surging chip stock in particular: Marvell Technology (MRVL). The AI infrastructure story is real, the custom silicon wins are real, and the stock's leadership reflects genuine fundamental momentum. But heading into Tuesday's earnings print after the bell, I'm not chasing it.MRVL sits at the intersection of hyperscaler capex and custom ASIC demand — two of the most powerful secular tailwinds in tech. Institutional money has rotated hard into the name, and the price action shows it; up more than 130% year-to-date and more than 220% over the past 52 weeks.Stock Chart IconStock chart iconMarvell Technology, 1 yearThe issue I have is that the rally has continued unabated. As I write this, MRVL has just hit another new high, and the 14-day RSI is above 70 (albeit not as high as it was recently), indicating that the pace of relative outperformance is slowing. While that's not a sell signal on its own, in a name that's already had an enormous run, it does beg the question: how much is already priced in? Notice how far above the long-term moving average MRVL is now (upper chart) and relatively elevated options premiums are now (lower chart)*The options market is pricing an ~13.5% move by the end of the week, far larger than the decade-long average earnings swing of 8.5%."Admittedly, the more recent 8-quarter average of ~11.75% is closer to what the straddle currently prices, so yes, MRVL has shown it can deliver outsized moves. But stacking a near-20% rally on top of an already extended chart? That's a much harder ask.Meanwhile, the forward P/E has climbed to approximately 45x — a 10-year high for this name. And critically, it's arriving alongside the most aggressive revenue and earnings growth expectations we've seen over that same period. The setup demands execution. There's no margin for disappointment at these multiples.So here's my positioning: I want exposure to MRVL, but I want to get paid to wait for it at a better level. If the stock pulls back — or even just treads water after earnings — I want to own it at a discount. If it rips, I collect premium and move on.The tradeSell the MRVL June 5th weekly 162.5 Put @ $3.60. Strike is meaningfully below current levels, offering a comfortable buffer.Break-even on the downside: ~$158.90 at expiration.Max profit: full $3.60 premium if MRVL stays above $162.50 through June 5th.Skill Level: IntermediateStandstill yield: >2.2% in ~11 days. A 70% annualized yield is good if you can get it; in the worst-case scenario, you own the stock 19% lower. Our system highlights that a similarly structured trade in MRVL historically had a very high win rate (see below).This is a high-probability-of-profit structure. You're not betting on a blowout quarter — you're simply asserting MRVL doesn't fall sharply and stay down. Given the fundamental backdrop, that's a reasonable view. But the key discipline here is simple: don't buy it into earnings just because the story is good. Buy weakness. Don't chase strength.

Chip stocks continue to surge. Here's how to buy into the trend for less

Mike Khouw happens to like one surging chip stock in particular: Marvell Technology.

528 words~2 min read