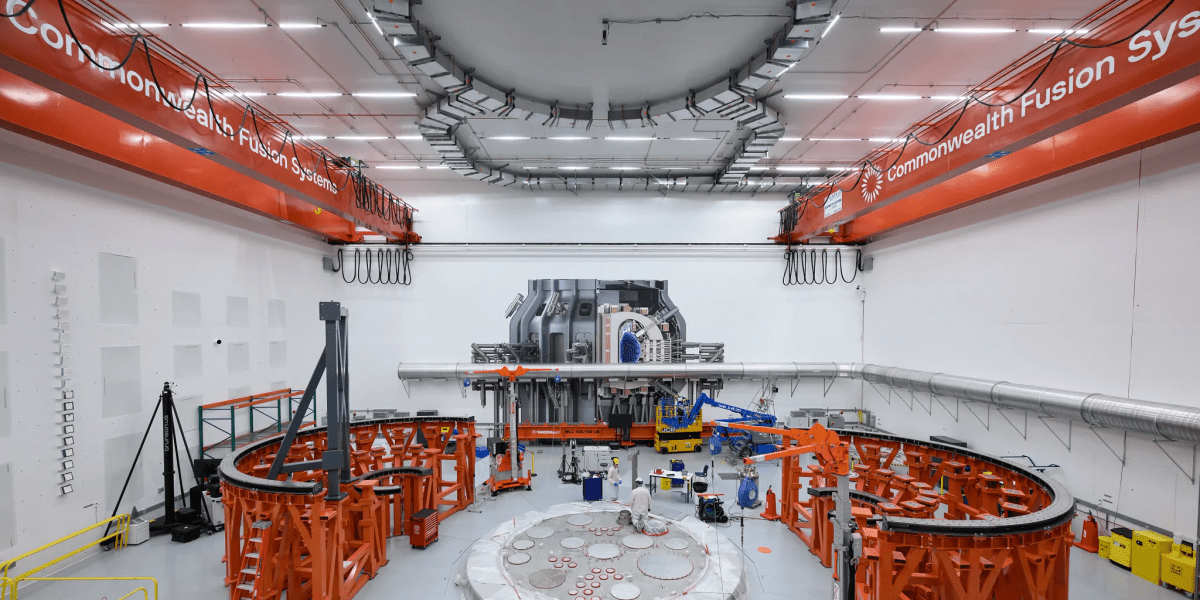

A new report from Canaccord Genuity captures the main threads from the firm’s first Nuclear Nexus conference, where fission and fusion developers, academics, and investors gathered to confront the practical barriers to scaling nuclear power. The event highlighted a shared recognition that surging electricity demand from AI data centers “finds itself bottle-necked by the physical reality of the grid”, forcing a hard look at fuel supply chains, regulatory timelines, and technology choices that can actually deliver power this decade.The forum set out to connect the established track record of fission with the still-developing promise of fusion. Participants framed the two paths as complementary: one centered on controlled separation to release energy at scale, the other on forcing materials together under extreme conditions to achieve the same goal. Canaccord’s summary presents this tension as more than rhetoric, noting that Western nuclear deployment has lagged for decades, while Asia and Russia have moved ahead, driving up costs and exposing fuel vulnerabilities.Oklo CEO Jacob DeWitte outlined the company’s Aurora Powerhouse, a liquid sodium-cooled fast reactor drawing on proven EBR-II technology and a build-own-operate model. He stressed the importance of securing a domestic HALEU supply chain through Idaho National Laboratory and Centrus, with longer-term options that include spent fuel reprocessing and access to government plutonium reserves suited to fast reactor designs. The discussion tied directly into broader concerns about Western dependence on foreign enriched uranium sources.MIT professor Jacopo Buongiorno highlighted how the lack of recent construction experience in the West has roughly doubled nuclear build costs compared with earlier decades. He noted that small modular reactors are more likely to provide financing flexibility than dramatically lower electricity costs, and that HALEU supply remains a critical chokepoint. The contrast with rapid expansion in Asia and continued Russian export dominance was presented as a structural challenge rather than a temporary setback.On the fusion side, UK Atomic Energy Authority’s Mike Gorley described the technology as fundamentally a large-scale thermal engineering problem rather than pure physics. A key constraint he flagged is the global shortage of Lithium-6, essential for tritium breeding and reactor performance. Several companies presented deployment timelines. Terra Innovatum’s SOLO microreactor is designed to run on either LEU or HALEU and incorporates inherent safety features that eliminate meltdown and explosion risks. The company is targeting a first-of-a-kind demonstration in 2027 and commercial units in 2028 under the NRC’s proposed Part 57 microreactor framework. Inertia is pursuing inertial confinement fusion and plans to begin construction of a 1.5 GW grid-scale plant in 2030 after solving manufacturing challenges for high-efficiency lasers and fuel targets. Newcleo is advancing lead-cooled fast reactors with MOX fuel and has partnered with Oklo to establish a U.S. MOX fabrication capability, addressing the domestic prohibition on commercial plutonium reprocessing.MIT professors Dennis Whyte and Andrew Lo described their new Rutherford Energy Ventures vehicle as a diversified portfolio approach across the fusion value chain. They cited easier regulatory pathways for fusion compared with fission and immediate revenue potential from spin-off technologies as reasons the sector could reach system-level integration within the next decade, aided by hyperscaler demand.TerraPower, backed by Bill Gates, received a landmark NRC construction permit in March 2026 for its Natrium sodium-cooled fast reactor in Wyoming. The company is on track for a 2030 startup and has signed a major agreement with Meta to develop up to eight additional Natrium units capable of supplying 4 GW of dispatchable power to data centers. Zap Energy is running a dual-track program that pairs a Z-pinch fusion reactor with a simpler sodium-cooled fission microreactor, planning to deploy the lower-risk fission technology in the early 2030s before scaling fusion later in the decade.Panels on critical materials and isotopes pointed to persistent supply constraints for both medical isotopes and nuclear fuel components that are expected to last through the 2020s due to underinvestment and lengthy permitting. ASP Isotopes is commercializing laser-based enrichment, SHINE Technologies is generating near-term revenue from isotope production and fusion-fission hybrids, and Uranium Energy Corp is positioning its U.S.-focused uranium assets against a projected 1.9-billion-pound market deficit.NuScale and its development partner ENTRA1 are advancing a six-plant deployment across the Tennessee Valley Authority territory, with four sites already identified. Participants noted that while evolutionary light-water designs are likely to lead near-term deployments, Generation IV reactors should play a larger role through the 2030s. Elementl framed itself as a technology-agnostic integrator focused on scaling proven light-water reactor projects to 100 GW by 2040 while hyperscalers such as Google provide early demand signals.The report leaves the impression that the nuclear sector is entering a more dynamic period, but one still defined by practical constraints on fuel, regulation, and execution speed rather than by any single breakthrough technology.

“We Must Leap Forward Into New Energy” - Canaccord’s Inaugural Nuclear Nexus Conference

The AI problem is an energy problem, and the industry needs to get serious about addressing it...

778 words~4 min read