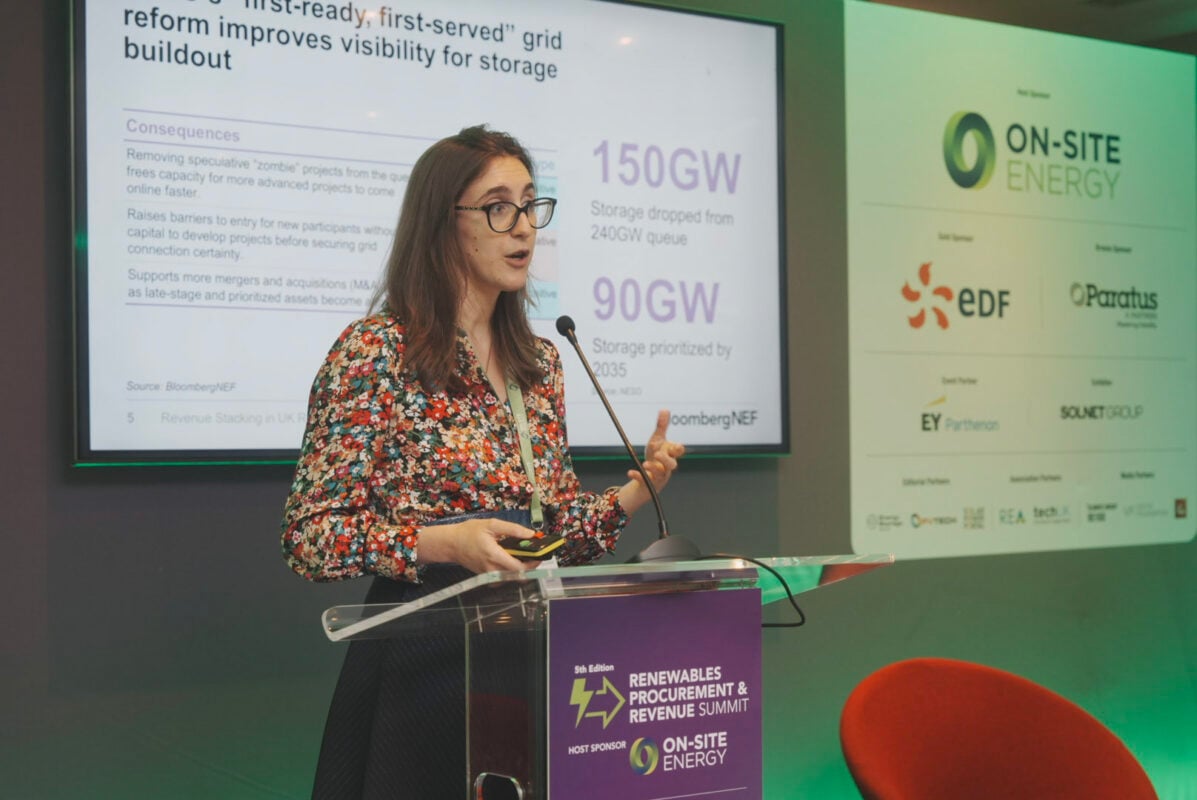

“It’s a global issue, but it’s been very predominant in Europe, in countries like Germany, Italy and the UK; we’ve seen very large grid connection queues, where a large portion of the queues are made up of storage projects,” she explained. “This directly eats into your project margins as your project is sitting there idle until it’s actually able to get connected.”

The diminishing of these delays, alongside a 31% year-on-year decline in turnkey BESS costs, means that developers may be financially incentivised to deploy batteries in the UK at present.

UK reaches BESS saturation

However, Grunenwald noted that the remaining connection queue backlog still exceeds the total volume of batteries that BloombergNEF expects to come online in the next decade, saying: “there’s still about 90GW that’s prioritised by 2035 [which is] still above what we expect to come online by that point.”

The batteries that do come online will also have to contend with complex market dynamics that require a similarly complicated revenue stack in order to turn a profit, not least because of the popularity of deploying new batteries in recent years; figures from Solar Media Market Research show that new utility-scale BESS capacity added in the UK has increased each year since 2017, as shown in the graph below.