On May 13, Fervo Energy went public at $27 a share and closed its first day of trading up 35%, pushing the company’s market capitalization past $10 billion. In the lead-up, demand was strong enough that Fervo increased the number of shares on offer and raised its asking price twice before the offering closed.

The customer book was anchored by the largest geothermal power purchase agreement ever signed: for a 320-megawatt deal with Southern California Edison, for power from Fervo’s under-construction Cape Station project in Utah.

It’s certainly the most significant commercial milestone in U.S. geothermal history. The $1.89-billion offering gave an industry that had operated for two decades as a series of pilot projects and government cost-share grants a publicly traded flagship.

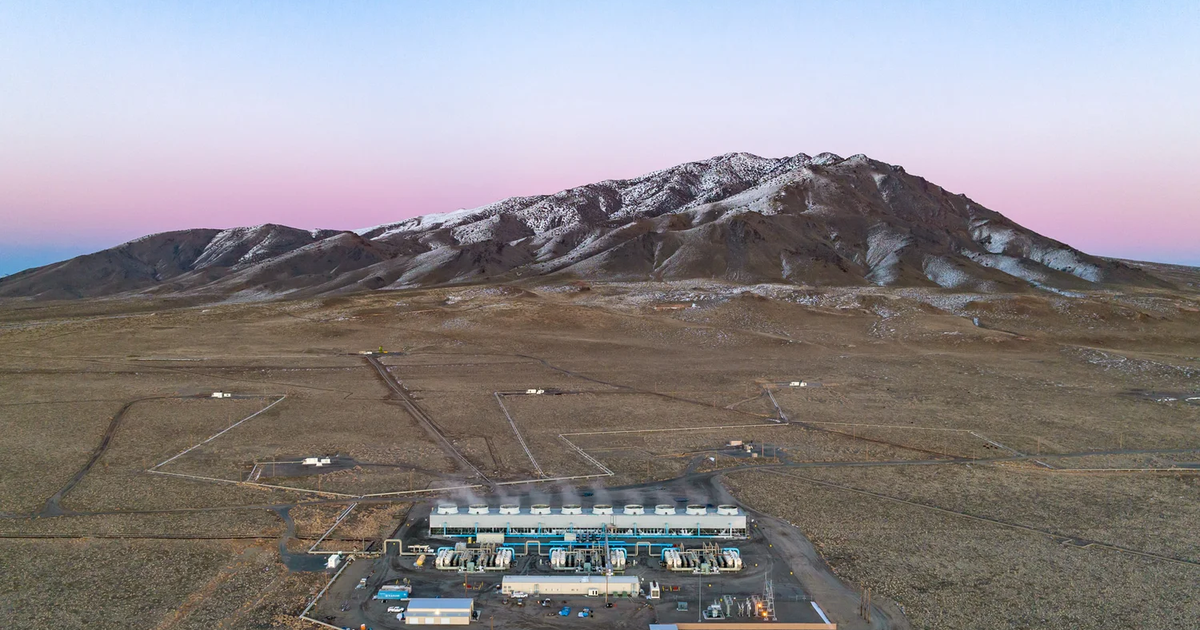

Hyperscaler demand has made clean baseload capacity a scarce resource in the U.S. data center buildout. Fervo had spent the prior eighteen months signing contracts to deliver exactly that, including a 115-MW agreement with Google for its Corsac Station project in Nevada that also yielded the hyperscaler’s “clean transition tariff,” a novel incentive model to get emerging clean energy projects built.

However, what the IPO does not price is the dependency stack underneath Fervo’s success so far. These dependencies have a history of hitting capital-intensive energy technologies hardest at the moment of greatest enthusiasm. The most recent example is U.S. offshore wind, which at the height of its momentum in 2022 attracted $4.4 billion at a single federal lease auction.