Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

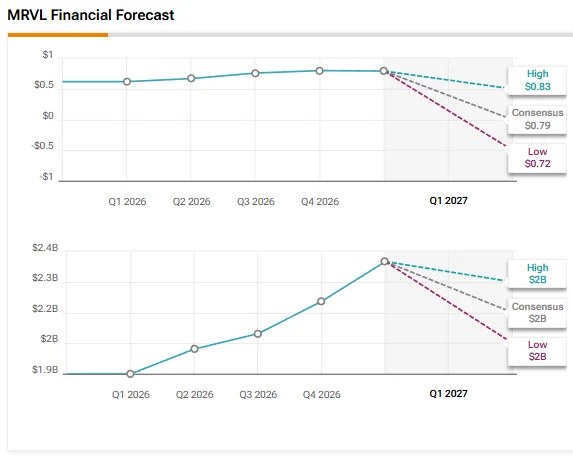

Meanwhile, Wall Street expects Marvell to report earnings per share (EPS) of $0.79 for Q1 FY27, implying 27.4% year-over-year growth. Revenue is estimated to rise by about 27% to $2.40 billion.

Analysts Are Optimistic on Marvell’s Growth Potential

Heading into Q1 FY27 results, RBC Capital analyst Srini Pajjuri reiterated a Buy rating on Marvell stock and increased his price target to $200 from $170. The 5-star analyst expects the momentum in MRVL’s optical business to continue through 2026. He views Nvidia’s recent investment as validation of Marvell’s dominance in the optical connectivity space. Pajjuri noted that custom XPU trends also appear strong, although near-term upside could be constrained by tight wafer supply.

Likewise, B. Riley analyst Craig Ellis reaffirmed a Buy rating on MRVL stock and raised his price target to $205 from $156. The 5-star analyst noted faster-than-anticipated acceleration in AI investment, driven by growing demand from hyperscalers and neo-cloud. This is boosting 2026-2028 capex estimates. Ellis added that new workload trends and major model providers are increasing chip intensity and tightening supply-demand dynamics. This supports strong semiconductor EPS revisions and high sector valuations despite recent volatility and comparisons to past technology cycles.