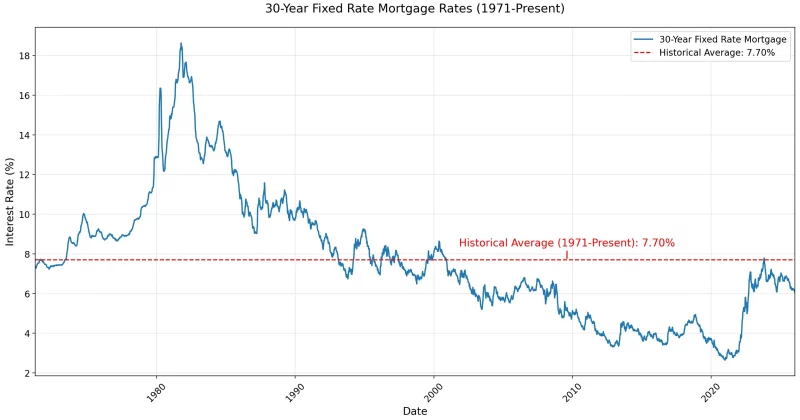

Mortgage refinance rates moved higher again on May 14, 2026, adding fresh pressure on homeowners hoping to lower monthly payments this spring. The average 30-year fixed refinance rate climbed to 6.54%, while 15-year refinance rates rose to 5.65%, according to new data from the Mortgage Research Center. At the same time, Zillow lender marketplace figures showed the broader 30-year mortgage rate rising to 6.34%, reflecting a sharp jump in Treasury yields and renewed market anxiety over inflation expectations.For millions of Americans, this shift is more than another financial headline. Mortgage refinance rates directly affect household budgets, long-term wealth building, and decisions about whether staying in a current loan still makes sense. After years of historically low borrowing costs during the pandemic era, homeowners are now navigating a market shaped by higher Federal Reserve policy rates, stubborn inflation pressures, and changing economic forecasts.Why are 30-year mortgage rates rising again in 2026The average 30-year fixed refinance rate increased to 6.54%, climbing 0.06 percentage points compared with last week. While that move may appear small, it significantly impacts lifetime borrowing costs for homeowners refinancing larger balances.The recent climb in refinance rates also reveals something deeper about the modern housing economy. Many borrowers locked in mortgages below 3% during 2020 and 2021. Today’s refinance rates above 6% create a difficult psychological and financial divide. Homeowners are no longer refinancing simply to reduce payments. Instead, many are refinancing to consolidate debt, tap home equity, or adjust loan terms to create longer-term financial flexibility.The housing market itself remains caught between competing forces. Inflation has cooled compared with previous years, but not enough to trigger aggressive Federal Reserve rate cuts. Treasury yields continue influencing mortgage pricing daily, and lenders remain cautious about long-term economic risks. That uncertainty is keeping refinance rates elevated even as many buyers and homeowners wait for relief.A homeowner refinancing a $100,000 mortgage at today’s 6.54% refinance rate would pay roughly $635 monthly in principal and interest. Over the life of the loan, total interest payments could reach approximately $129,276. Those numbers highlight how elevated refinance rates continue reshaping affordability across the housing market.The broader mortgage market also reflected rising pressure. According to Zillow lender marketplace data, the standard 30-year fixed mortgage rate climbed to 6.34%, marking the highest single-day increase since late March. Analysts tied the jump largely to rising 10-year Treasury yields, which heavily influence mortgage pricing across the United States.What makes this moment particularly important is the contrast with recent history. Just a few years ago, refinance rates near 2.75% were common. Today’s rates above 6% represent a dramatically different borrowing environment. That shift has slowed refinance activity nationwide while forcing homeowners to rethink financial strategies once considered automatic.Why are mortgage refinance rates climbing in 2026?Mortgage refinance rates are climbing because investors increasingly believe inflation may remain persistent longer than expected. Financial markets closely monitor Federal Reserve policy signals, employment data, and Treasury yields, all of which influence mortgage pricing daily.When Treasury yields rise, lenders typically raise mortgage refinance rates to offset higher borrowing costs and long-term financial risk. This week’s increase in the 10-year Treasury yield pushed lenders to adjust rates upward almost immediately.The Federal Reserve remains central to the story. Although inflation has cooled from its earlier peaks, policymakers continue signaling caution about cutting interest rates too aggressively. If inflation remains stubborn while unemployment stays low, mortgage rates may remain elevated through much of 2026.Economists increasingly describe the current mortgage environment as a “higher-for-longer” cycle. Rather than expecting dramatic rate collapses, borrowers may need to adjust to a slower decline pattern shaped by inflation data, labor market trends, and Federal Reserve decisions throughout the year.15-year refinance rates versus 30-year mortgage refinance ratesThe average 15-year fixed refinance rate climbed to 5.65%, up from 5.56% last week. Although monthly payments are higher with shorter-term loans, borrowers typically save substantial amounts in total interest over time.At today’s rates, refinancing a $100,000 loan into a 15-year mortgage would cost approximately $825 monthly in principal and interest. However, total lifetime interest would fall dramatically to around $48,954. That difference explains why financially stable borrowers often prefer shorter loan terms despite higher monthly obligations.Meanwhile, 20-year refinance rates averaged 6.42%, creating a middle-ground option for homeowners balancing affordability with long-term savings. A borrower refinancing $100,000 into a 20-year fixed mortgage would pay roughly $741 monthly while spending about $78,429 in total interest.The emotional side of refinancing often receives less attention, yet it matters deeply. Many homeowners today are weighing certainty against flexibility. A 30-year refinance offers lower monthly payments and breathing room during uncertain economic conditions. A 15-year refinance provides faster debt freedom and lower overall interest costs.Choosing between these options depends heavily on personal financial priorities. Borrowers focused on cash flow may favor longer terms. Those prioritizing wealth building and retirement preparation may lean toward shorter refinance structures.Should homeowners refinance now or wait for lower mortgage rates?The biggest question facing homeowners today is whether refinancing now makes sense or whether waiting could lead to better mortgage refinance rates later in 2026.The answer depends less on predicting markets and more on understanding personal financial goals. Some experts suggest refinancing becomes worthwhile when borrowers can reduce their rate by at least 1% or even 2%. However, that traditional rule no longer fits every financial situation.For homeowners carrying high-interest debt, refinancing may still offer benefits through cash-flow management or debt consolidation. Others may refinance to switch from adjustable-rate mortgages into fixed-rate stability before future market volatility emerges.Still, closing costs remain a major consideration. Refinancing generally includes fees ranging from 2% to 6% of the loan amount, including appraisal costs, lender charges, and title-related expenses. Borrowers must calculate the “break-even point” — the time required for monthly savings to outweigh upfront refinance costs.

Mortgage rates today jump sharply: Is the hidden Treasury yield surge making 2026 home refinancing painfully expensive for Americans?

Mortgage rate today climbs as Treasury yields jump and refinance pressure returns across the US housing market. The average 30-year fixed refinance rate rose to 6.54%, while standard 30-year mortgage rates touched 6.34%. Rising bond yields, sticky inflation, and cautious Federal Reserve signals are now pushing borrowing costs higher again. Homeowners who once waited for lower mortgage refinance rates are facing a different reality in todays market.

954 words~4 min read