As Gen Z awaits its share of the $124 trillion Great Wealth Transfer from their baby boomer relatives, the generation’s financial footing is being put to the test.

Typically, younger consumers see the fastest year-over-year gains in credit scores as they build their financial histories. But this year, the opposite happened: Gen Z just experienced the steepest annual drop of any age group since 2020, with their average FICO credit score slipping three points to 676. That’s 39 points lower than the national average of 715, according to a new FICO report.

The decline is a “red flag,” said Erin Stillwell, head of payments at Globant—not only for young consumers, but for the health of the broader credit market.

“Today’s young adults borrow just to reach baseline stability, not luxury,” she told Fortune. “The decline reflects a generation building financial identity in a system that rewards stability but gives volatility.”

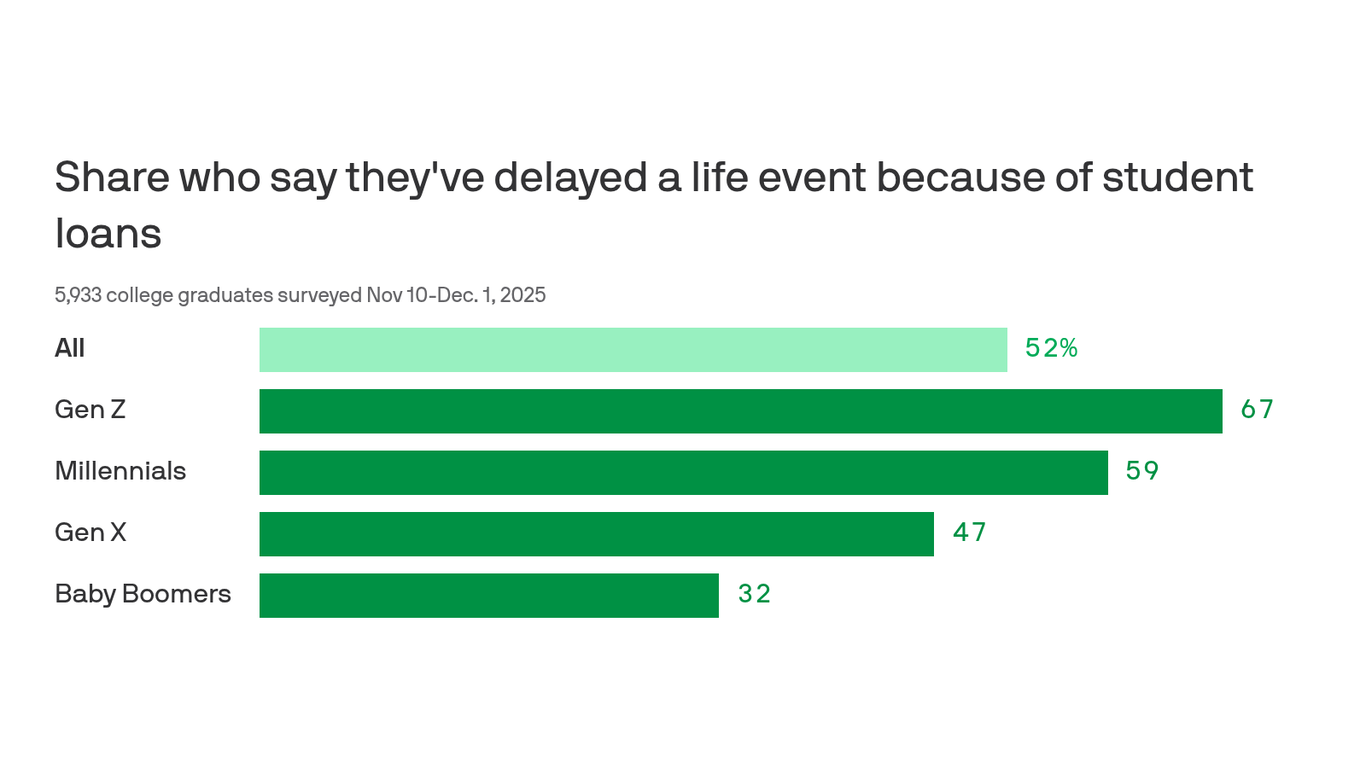

And that volatility is piling up. Gen Z is more likely to feel the sting of stubborn inflation and high interest rates. With less time to build savings, invest in the stock market, or benefit from home appreciation, they’re already on shakier financial ground than their older counterparts. Add in the return of student loan payments and the rise of “doomspending”—the impulse to spend as a way with financial anxiety—and it’s become a perfect storm.